How Delinquency Trends Reorient Canada’s Auto Loan Market

Team at Bill Gosling🔄 Last Updated: January 27, 2026

Introduction

We are witnessing a significant shift taking place across the Canadian auto loan market- and it’s occurring one missed payment at a time. Previously, the missed payments were a manageable risk metric; however, now it has become an impactful warning of severe financial stress. Delinquency trends are not indicators of who’s lagging; they project in real time the reconstruction of affordability, credit behaviour, and lender strategy.

1. Rising Delinquencies are an Indicator of Financial Stress

It has been observed in the latest credit data that the delinquency rates on non-mortgage credit, including auto loans, have increased strongly. It has reached the extent that was not noticed since the financial crisis of 2008. A press release by Equifax – Delinquency Levels Show Signs of Stabilizing, But The Financial Gap Continues To Widen For Some Canadians– reported that in Q3 2025, more than 1.45 million payments were missed by Canadians[ii]

.

If we talk about demography and regions, the younger population, i.e., under 36 years of age, is more vulnerable and reports soaring delinquency in comparison to the older groups. This increase is attached to the impediments attached to modifications in the job sector and the higher cost of living.

2. Specific pressure in Auto Loans

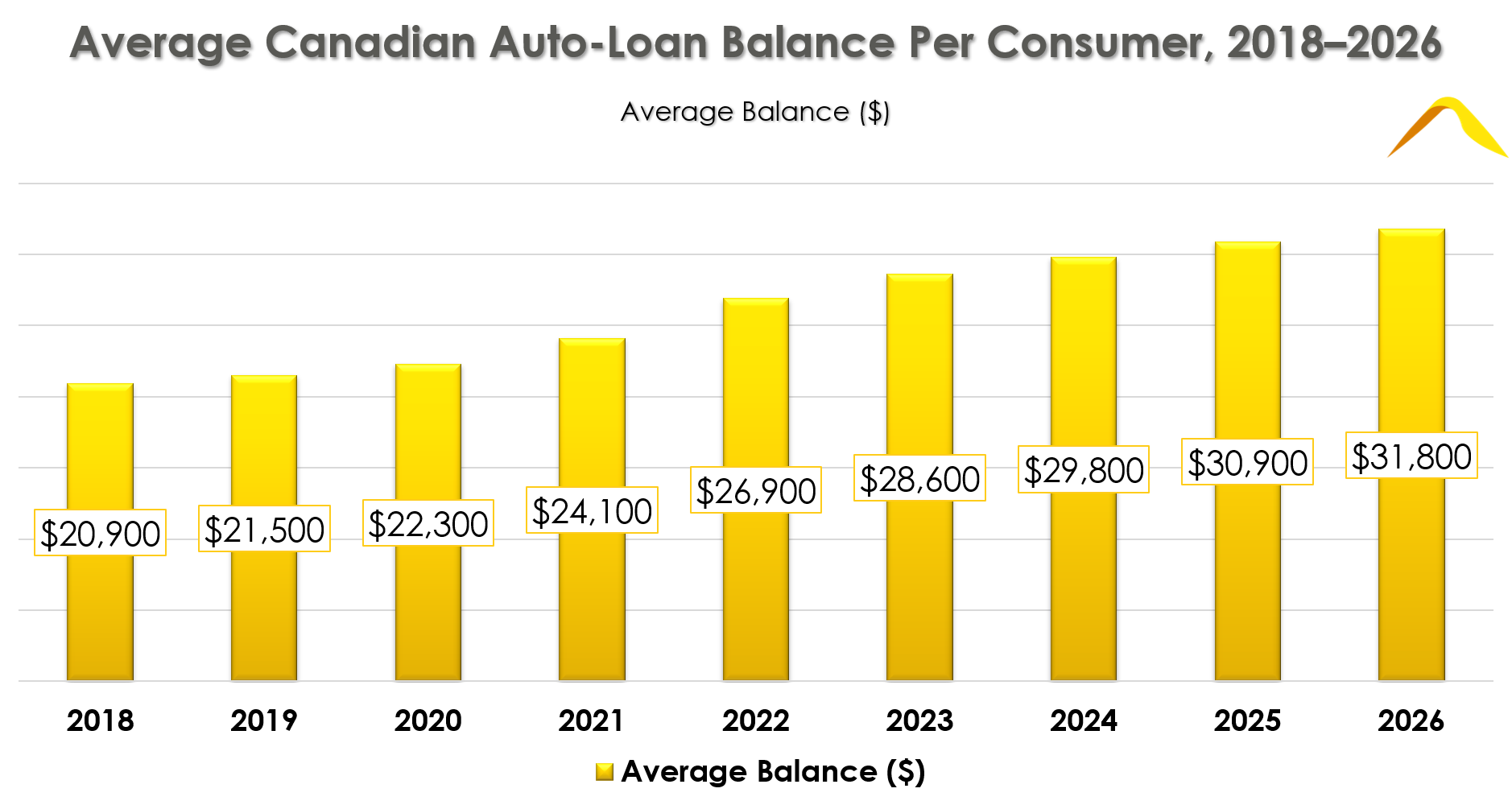

A distinct stress is observed in auto loan especially among near-prime and subprime borrowers.

Past-due rates for auto loans (e.g., 60+ days past due) have increased above the pre-pandemic standards. This exhibits a market where pressure is experienced by even the creditworthy section.

Subprime auto loan delinquencies, such as 60-day+ past due figures, have increased to unprecedented levels, indicating severe stress among a section of borrowers that is high risk.

3. What’s enabling the Delinquency Trend?

• Cost-of-living crisis

The high prices of vehicles, the bull-headed elevated rate of interest, and cost-of-living constraints have pushed the monthly payments. This has extended the payment across longer loan terms.

• Expansion of borrower number

New-to-credit consumers, who comprise immigrants and younger adults. Delinquent within the first year of credit usage, this section of the population is rising in numbers, and as per data, their probability of turning delinquent within the first year of credit usage is higher.

The average non-mortgage debt rose to $14,304 for Canadians under the age of 36 in Q2 2025. Also, there was an intense surge in the 90+ day delinquency rates to 2.35%, which was 1.3% increase from the last quarter

Reinforcing Underwriting

The credit criteria are reinforced by the lenders to recalibrate risk, specifically for the contentious credit profiles, as stats proved that these profiles are risk prone.

Conclusion- A plunge towards Resilient Auto Lending

A reorganization of Canada’s auto loan market is being done. This reorientation is not happening just because of the consumer behaviour, but by the transformation of the character of the credit risk itself. Delinquency trends have ceased to be just uproar and have become a prominent indicator for lenders, dealers, and financial institutions to act.

By adopting a risk assessment that is driven by data, an empathetic borrower engagement, and technological advancement, the market can thrive in even a situation of increased delinquency dynamics.

Frequently Asked Questions on Auto Loan Delinquency Trends in Canada

1. What is the relevance of delinquency trends in Canada’s auto loan market?

Delinquency trends act as an early indicator of financial strain. As the cost of living rises, missed or delayed payments signal growing challenges for borrowers and highlight lenders where credit risk is increasing.

2. Which borrower segments are most affected by rising auto loan delinquencies?

The borrower segments showing higher delinquency rates include:

Younger borrowers under 36 years of age

Near-prime and subprime borrowers

Borrowers impacted by higher living costs

3. Does technology play a role in managing auto loan delinquencies?

Yes. Technologies such as advanced analytics, AI-driven risk scoring, and real-time monitoring help lenders identify at-risk accounts early. This enables proactive outreach and the offering of flexible repayment options.

4. What steps should lenders adopt in the future to manage delinquencies?

Lenders should focus on the following steps:

Early identification of credit risk

Flexible and customer-centric repayment strategies

Strong, analytics-driven monitoring frameworks

A balanced approach to risk control and borrower engagement